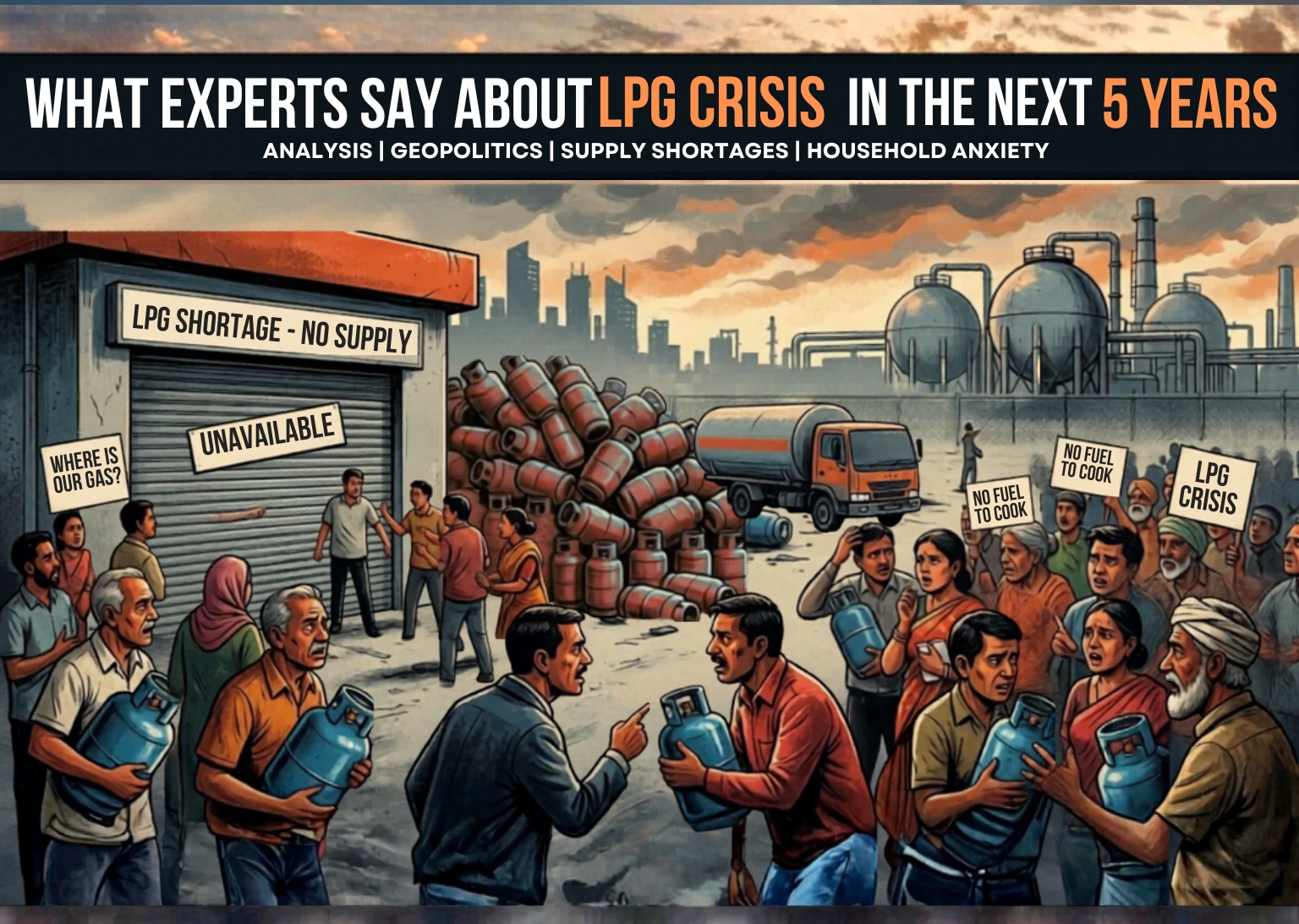

The global Liquefied Petroleum Gas (LPG) panorama is getting into a duration of remarkable volatility. While the gasoline has lengthy been celebrated as a “bridge” to purifier power—imparting a decrease carbon footprint than coal and wood—the next 5 years (2026–2031) are projected to be defined by way of a series of “mini-crises” rooted in geopolitical instability, infrastructure bottlenecks, and a fast, forced shift in the direction of electrification.

Industry analysts and electricity experts are sounding the alarm on 3 particular fronts: the “Hormuz Hazard,” the storage deficit in emerging markets, and the competitive cannibalization of LPG call for by piped natural gasoline and induction cooking.

The Geopolitical Chokepoint: A 2026 Reality Check

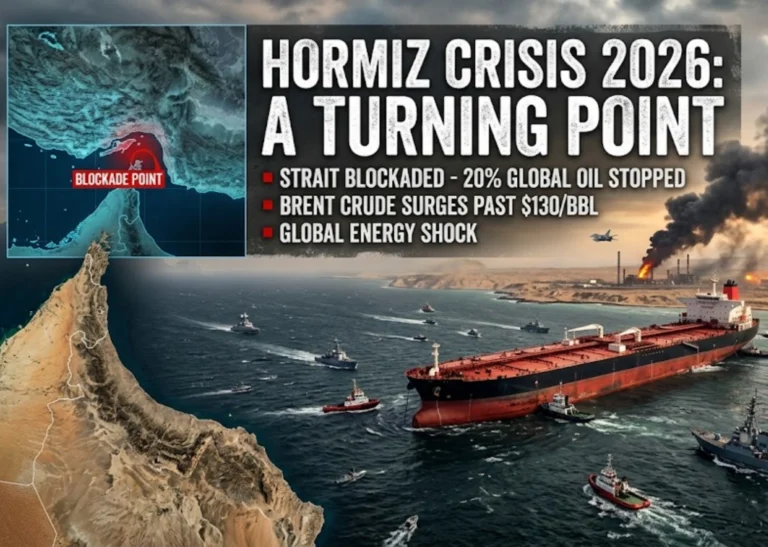

As of early 2026, the primary driving force of the immediately LPG disaster is the heightened tension in West Asia. Experts point to the Strait of Hormuz as the unmarried most considerable vulnerability in the worldwide supply chain. Roughly 35% of all globally traded LPG transits via this narrow waterway.

With current disruptions in the location, spot costs have surged considerably. Analysts from groups like S&P Global and Argus Media observe that even without a total blockade, the “war-hazard” charges delivered through insurers have made transport from Qatar, the UAE, and Saudi Arabia prohibitively expensive for fee-sensitive markets like India and Southeast Asia. This has triggered a “forced diversification,” in which nations are desperately seeking lengthy-haul cargoes from the U.S. Gulf Coast, in addition straining the global fleet of Very Large Gas Carriers (VLGCs).

The Storage Gap: Living “Hand-to-Mouth”

An ordinary subject matter among power strategists is the dangerous lack of Strategic Petroleum Reserves (SPR) for LPG, specifically compared to crude oil. In many developing countries, LPG intake has tripled over the past decade because of a hit smooth-cooking initiatives like India’s Ujjwala Yojana. However, garage infrastructure hasn’t stored tempo.

- Current Reality: Most essential importers currently keep the handiest 25–30 days of operational inventory.

- Expert Consensus: To tell the tale of the next 5 years of volatility, professionals argue that countries have to construct underground salt caverns or big-scale refrigerated tanks able to maintain at least 60–90 days of intake.

- The Cost Barrier: Building those centers is capital-in depth and technically tough. Without “quasi-strategic” mandates—wherein importers are compelled to keep minimum buffers—the marketplace remains susceptible to every minor shipping postpone or refinery outage.

The Petrochemical Pivot vs. Residential Demand

One of the most complex dynamics for the following 5 years is the inner “conflict” for propane and butane. While families rely on LPG for survival, the petrochemical enterprise—specially in China and India—is eating it at report rates as a feedstock for plastics.

China’s Propane Dehydrogenation (PDH) ability has reached over 22 million tonnes in keeping with yr. Experts endorse that when business demand and home demand collide for the duration of top iciness months, the “crisis” isn’t always a lack of gas, but a loss of low-priced fuel. Industrial gamers can frequently outbid authorities-subsidized family applications, main to localized shortages or ballooning financial deficits for governments seeking to maintain cylinder prices strong.

The “Great Switch”: A Forced Energy Transition

Perhaps the most telling professional prediction is that the LPG disaster will truly accelerate its very own loss of life in city areas. Government officials in numerous countries have already began imparting incentives for “LPG Alternatives” to mitigate deliver dangers.

1. Piped Natural Gas (PNG)

In urban centers, the push is in the direction of “Cylinder-Free” cities. By laying widespread pipeline networks, governments desire to shift the weight far from the complex logistics of LPG bottling and trucking. Analysts count on a 6% to 8% CAGR in PNG growth via 2031, without delay carving out the most worthwhile market segments from LPG distributors.

2. The Rise of Electric Induction

For the primary time, electric induction cooking is being framed no longer simply as a “green” preference, however as a “security” desire. With LPG fees soaring at ancient highs, the value of cooking with power has come to be competitive in lots of areas. Experts predict that the electric cooking phase will grow with the aid of over 10% yearly through 2031, as families seek to insulate themselves from the “rollercoaster” of worldwide gas markets.

Supply-Side Hope: The U.S. And Qatari Expansions

While the outlook for prices is grim, the “crisis” is not necessarily considered one of general worldwide shortage. The U.S. Continues to break export information, and Qatar’s North Field growth is slated to convey large new volumes online with the aid of mid-to-past due 2026.

The bottleneck, professionals warn, is logistics. Even if the fuel exists in Texas or Doha, the arena lacks the “last-mile” resilience—the ships, the port-facet terminals, and the local storage—to make sure that a crisis in one a part of the sector doesn’t trigger a blackout in another. The subsequent 5 years may be a race among expanding this infrastructure and a worldwide patron base this is an increasing number of searching out the go out door.

Read More:- How Supply and Demand Control Crude Oil Prices